Stat 435 Lecture Notes 3

Xiongzhi Chen

Washington State University

Linear regression with a qualitative predictor

Motivation

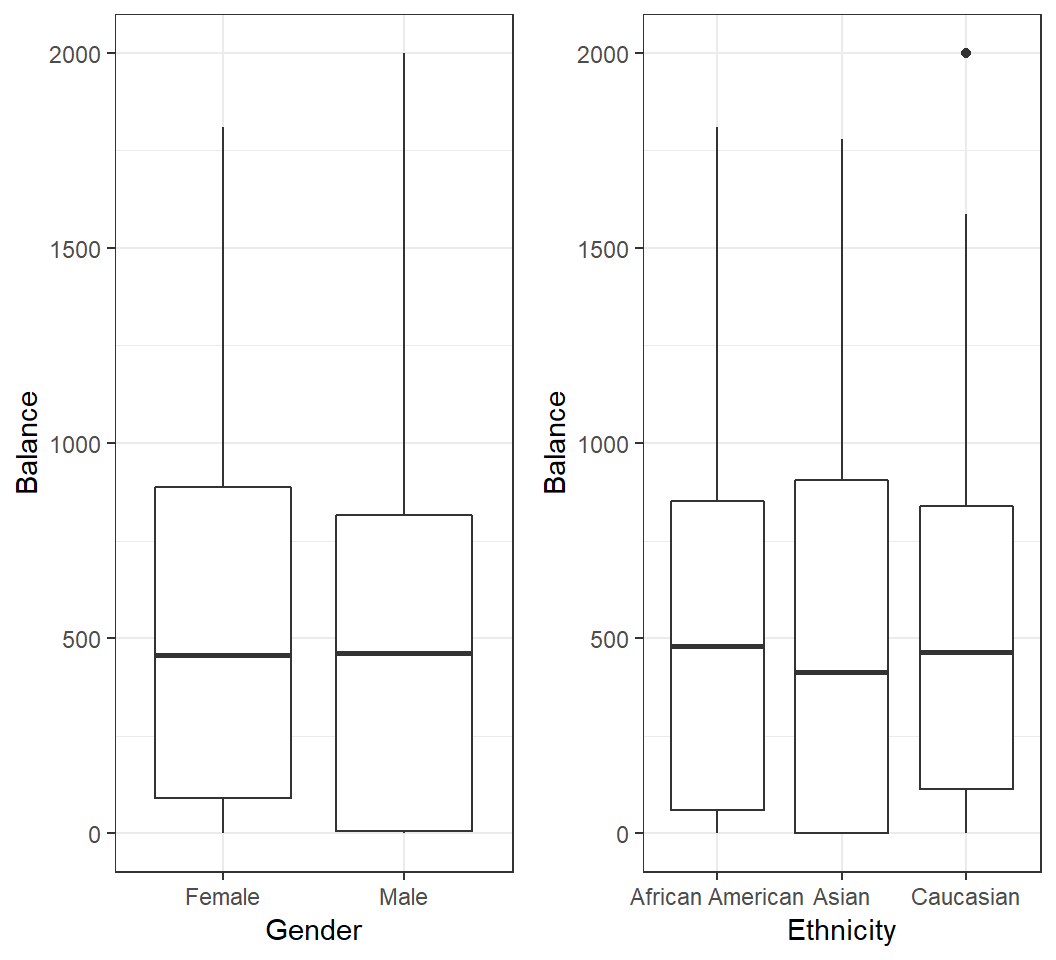

How is

Balanceof a credit card related to a user’sGender?How is

Balanceof a credit card related to a user’sEthnicity?

Motivation

Model 1: 2 levels

- Coding:

Genderhas 2 levels,MaleandFemale - dummy variable: \(x_i =0\) if \(i\)th person is

Femaleand \(x_i =1\) if \(i\)th person isMale - Model: \(y_i = \beta_0 + \beta_1 x_i + \varepsilon_i\), which induces 2 submodels:

- \(y_i = \beta_0 + \beta_1 + \varepsilon_i\) if \(i\)th person is

Male - \(y_i = \beta_0 + \varepsilon_i\) if \(i\)th person is

Female

Note: dummy variable follows coding by R, for which the first level Female is the baseline

Model 1: 2 levels

Model: \(y_i = \beta_0 + \beta_1 x_i + \varepsilon_i\)

- \(x_i =0\) if \(i\)th person is

Female, and \(x_i =1\) if \(i\)th person isMale - \(\beta_0\): average

Balancefor females - \(\beta_1\): average difference in balance between males and females

Remark: coding of a dummy variable is arbitrary and should be easily interpretable

Fitting the Model 1

Call:

lm(formula = Balance ~ Gender, data = creditData)

Coefficients:

(Intercept) GenderMale

529.54 -19.73 Females have an averagebalanceof $529.54;FemalebaselineMales have an averagebalanceof $(529.54-19.73)= $509.80

Note: in R, by default the first level Female is the baseline

Testing the Model 1

Call:

lm(formula = Balance ~ Gender, data = creditData)

Residuals:

Min 1Q Median 3Q Max

-529.54 -455.35 -60.17 334.71 1489.20

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 529.54 31.99 16.554 <2e-16 ***

GenderMale -19.73 46.05 -0.429 0.669

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 460.2 on 398 degrees of freedom

Multiple R-squared: 0.0004611, Adjusted R-squared: -0.00205

F-statistic: 0.1836 on 1 and 398 DF, p-value: 0.6685- If model assumptions are met,

Genderis not significant on affecting averagebalanceat type I error level 0.05 based on F-statistic (or the p-value ofGenderMale)

Model 2: 3 levels

Ethnicity has 3 levels African American (1st level and baseline in R), Asian, and Caucasian. 2 dummy variables are needed:

- \(x_{i1} =0\) if \(i\)th person is not

Asian, and \(x_{i1} =1\) if \(i\)th person isAsian - \(x_{i2} =0\) if \(i\)th person is not

Caucasian, and \(x_{i2} =1\) if \(i\)th person isCaucasian - Model: \[y_i = \beta_0 + \beta_1 x_{i1} +\beta_2 x_{i2} + \varepsilon_i\]

Model 2: 3 levels

Model: \[y_i = \beta_0 + \beta_1 x_{i1} +\beta_2 x_{i2} + \varepsilon_i\]

- Codings on previous slide

- \(\beta_0\): average

balanceforAfrican American - \(\beta_1\): average difference in

balancebetweenAsianandAfrican American - \(\beta_2\): average difference in

balancebetweenCaucasianandAfrican American

Fitting the Model 2

Call:

lm(formula = Balance ~ Ethnicity, data = creditData)

Coefficients:

(Intercept) EthnicityAsian EthnicityCaucasian

531.00 -18.69 -12.50 African Americans have an averagebalanceof $531Asians have an averagebalanceof $(531-18.69)= $512.31Caucasians have an averagebalanceof $(531-12.50)= $518.5

Testing the Model 2

Call:

lm(formula = Balance ~ Ethnicity, data = creditData)

Residuals:

Min 1Q Median 3Q Max

-531.00 -457.08 -63.25 339.25 1480.50

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 531.00 46.32 11.464 <2e-16 ***

EthnicityAsian -18.69 65.02 -0.287 0.774

EthnicityCaucasian -12.50 56.68 -0.221 0.826

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 460.9 on 397 degrees of freedom

Multiple R-squared: 0.0002188, Adjusted R-squared: -0.004818

F-statistic: 0.04344 on 2 and 397 DF, p-value: 0.9575If model assumptions are met, at type I error level 0.05, Ethnicity does not significantly affect average balance based on the F-statistic

Testing the Model 2

# A tibble: 3 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 531. 46.3 11.5 1.77e-26

2 EthnicityAsian -18.7 65.0 -0.287 7.74e- 1

3 EthnicityCaucasian -12.5 56.7 -0.221 8.26e- 1If model assumptions are met and Ethnicity does not significantly affect average balance, there is no need to check

- whether there is significant difference in average

balancebetweenAsians andAfrican Americans or betweenCaucasians andAfrican Americans

Diagnostics

Diagnostics are the same as those for simple linear regression with a quantitative predictor.

Multiple linear regression

Motivation

How is

sales(in thousands of units) for a particular product related to advertising budgets (in thousands of dollars) forTV,radioandnewspaper?Model:

sales= \(\beta_0\) + \(\beta_1 \times\)TV+ \(\beta_2\times\)radio+ \(\beta_3 \times\)newspaper+ \(\varepsilon\)

We want to examine the relationship between sales and budgets for TV, radio and newspaper jointly, instead of marginally.

Model

Response \(Y\) and \(p\) predictors \(X_1, X_2, \ldots, X_p\), bound by model

\[Y = \beta_0 + \beta_1 X_1 +\beta_2 X_2 + \cdots + \beta_p X_p + \varepsilon\]

\(\beta_j\): change in units in \(E(Y)\) for a unit change in \(X_j\) while holding all other predictors fixed

\(\varepsilon\): random error term with \(E(\varepsilon)=0\) and \(Var(\varepsilon)=\sigma^2\)

Estimate coefficient vector \(\boldsymbol{\beta}=(\beta_0,\beta_1,\ldots,\beta_p)\) by the least squares method; estimate \(\hat{\boldsymbol{\beta}}=(\hat{\beta}_0,\hat{\beta}_1,\ldots,\hat{\beta}_p)\) as LSE (least squares estimate)

Fitting model

Joint model vs marginal model:

# A tibble: 4 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 2.94 0.312 9.42 1.27e-17

2 TV 0.0458 0.00139 32.8 1.51e-81

3 radio 0.189 0.00861 21.9 1.51e-54

4 newspaper -0.00104 0.00587 -0.177 8.60e- 1# A tibble: 2 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 12.4 0.621 19.9 4.71e-49

2 newspaper 0.0547 0.0166 3.30 1.15e- 3# A tibble: 2 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) 7.03 0.458 15.4 1.41e-35

2 TV 0.0475 0.00269 17.7 1.47e-42Testing on all coefficients

- Is there a relationship between the response and any of the predictors? Namely, is \(H_0: \beta_1=\beta_2=\cdots=\beta_p=0\) true?

- Test statistic: F-statistic \[F=\frac{(TSS-RSS)/p}{RSS/(n-p-1)},\] where \(TSS=\sum_{i=1}^n (y_i - \bar{y})^2\) with \(\bar{y}=n^{-1}\sum_{i=1}^n y_i\) and \(RSS=\sum_{i=1}^n (y_i - \hat{y}_i)^2\)

- If \(H_0\) is true and the linear model assumptions are correct, F-statistic should be close to 1 on average; under suitable conditions, F-statistic approximately follows an F-distribution

Testing on all coefficients

Testing \(H_0: \beta_1=\beta_2=\cdots=\beta_p=0\):

value numdf dendf

570.2707 3.0000 196.0000

value

1.575227e-96 F-statistic: 570.3 with numerator degrees of freedom 3 and denominator degrees of freedom 196; p-value: < 2.2e-16

- Conclusion: reject \(H_0\), meaning that at least one of the predictors has a relationship with the response.

Testing on some coefficients

Is there no relationship between the response and some predictors? Namely, for some \(1 \le q \le p\), test \[H_0: \beta_{p-q+1}=\beta_{p-q+2}= \ldots = \beta_{p}=0\]

- Fit \(M_0: Y = \beta_0 + \beta_1 X_1 + \ldots + \beta_{p-q} X_{p-q} + \varepsilon\), and obtain its residual sum of squares \(RSS_0\)

- Fit \(M_1: Y = \beta_0 + \beta_1 X_1 + \ldots + \beta_{p-q} X_{p-q} + \ldots + \beta_p X_p+\varepsilon\), and obtain its residual sum of squares \(RSS\)

- Use test statistic \[F = \frac{(RSS_0 - RSS)/q}{RSS/(n-p-1)}\]

Testing on some coefficients

When \(H_0\) and model assumptions are true, test statistic \[F = \frac{(RSS_0 - RSS)/q}{RSS/(n-p-1)}\] approximately follows an F-distribution with numerator degrees of freedom \(q\) and denominator degrees of freedom \(n-p-1\)

Testing on model fit

- \(R^2\) measures the proportion of variance that is explained by the postulated model

- With three predictors:

> FitL3c = lm(sales~TV+radio+newspaper,data=adData)

> summary(FitL3c)$r.squared

[1] 0.8972106- With one predictor:

> FitL3d = lm(sales~newspaper,data=adData)

> summary(FitL3d)$r.squared

[1] 0.05212045Interaction terms

Interaction terms: I

Consider predicting the average sales (in thousands of dollars) via budgets in advertisement through TV and Radio.

Model 1: \(E\)(

sales) = \(\beta_0\) + \(\beta_1 \times\)TV+ \(\beta_2 \times\)RadioModel 1: how is the change (in unit) in \(E\)(

sales) relates to a unit change inTVand/orRadio?Is model 1 sensible when changes (in unit) in \(E\)(

sales) are different for a unit change inTVwhenRadiotakes different values?

Interaction terms: I

- If change (in unit) in \(E\)(

sales) can be different for a unit change inTVat different values ofRadioor for a unit change inRadioat different values ofTV, then the model \[ E(\textsf{sales}) = \beta_0 + \beta_1 \times\textsf{TV} + \beta_2 \times\textsf{Radio} \] is no longer suitable

- One way to account for this is to introduce an interaction term and use model \[ E(\textsf{sales}) = \beta_0 + \beta_1 \times \textsf{TV} + \beta_2 \times\textsf{Radio} + \beta_3 \times\textsf{TV} \times\textsf{Radio} \]

- Does the following model do the job? \[ E(\textsf{sales}) = \beta_0 + \beta_1 \times \textsf{TV} + \beta_2 \times \textsf{Radio} + \beta_3 \times \textsf{TV}^2+ \beta_4 \times \textsf{Radio}^2 \]

Interaction terms: I

The model \[ E(\textsf{sales}) = \beta_0 + \beta_1 \times \textsf{TV} + \beta_2 \times\textsf{Radio} + \beta_3 \times\textsf{TV} \times\textsf{Radio} \] can be written as \[ E(\textsf{sales}) = \beta_0 + \beta_1 \times \textsf{TV} + (\beta_2+ \beta_3 \times\textsf{TV})\times\textsf{Radio} \] or as \[ E(\textsf{sales}) = \beta_0 + (\beta_1 +\beta_3 \times\textsf{Radio})\times \textsf{TV} + \beta_2 \times\textsf{Radio} \]

Interaction terms: I

Fit the model with interaction:

Call:

lm(formula = sales ~ TV * radio, data = adData)

Residuals:

Min 1Q Median 3Q Max

-6.3366 -0.4028 0.1831 0.5948 1.5246

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 6.750e+00 2.479e-01 27.233 <2e-16 ***

TV 1.910e-02 1.504e-03 12.699 <2e-16 ***

radio 2.886e-02 8.905e-03 3.241 0.0014 **

TV:radio 1.086e-03 5.242e-05 20.727 <2e-16 ***

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 0.9435 on 196 degrees of freedom

Multiple R-squared: 0.9678, Adjusted R-squared: 0.9673

F-statistic: 1963 on 3 and 196 DF, p-value: < 2.2e-16Interaction terms: II

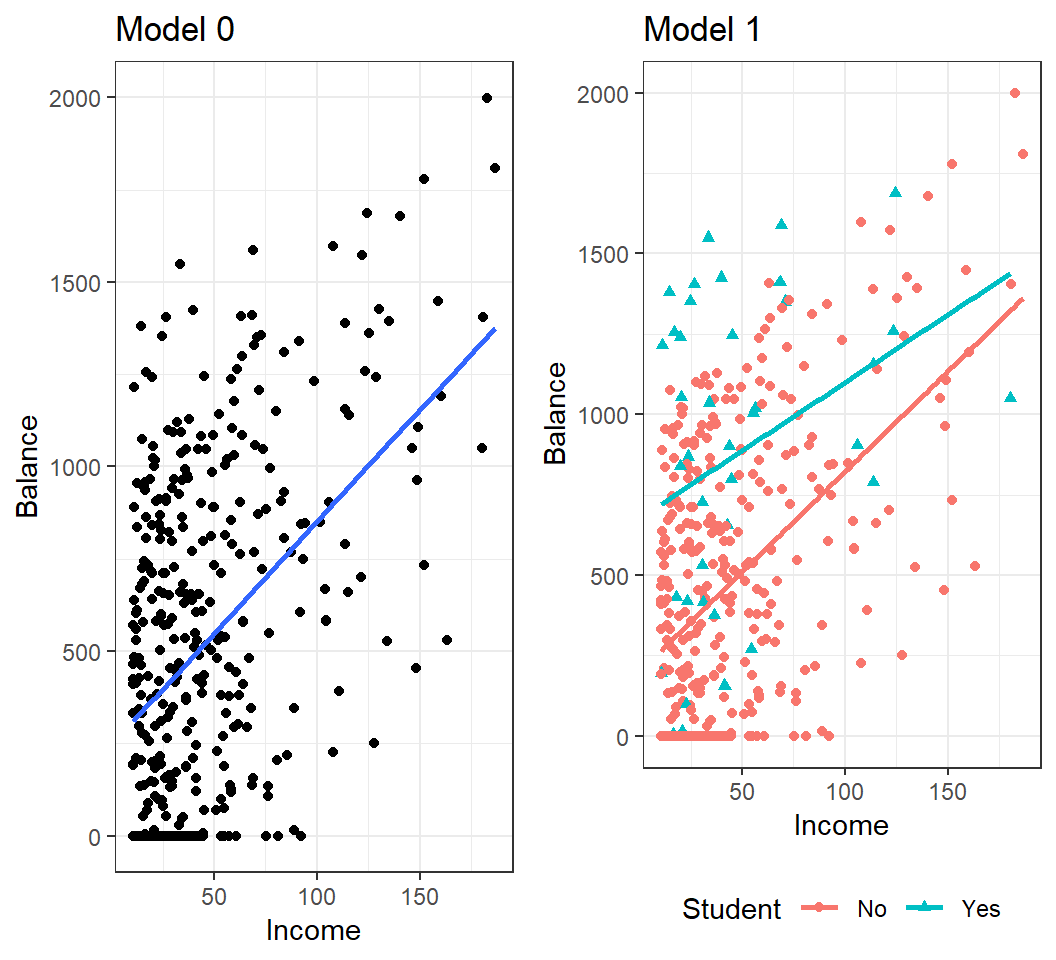

Consider predicting the average Balance (of a credit card) using information on if a user is a Student (“Yes” or “No”) and his/her Income

- Model 0: \(E\)(

Balance) = \(\beta_0\) + \(\beta_1 \times\)Income - Model 1: \(E\)(

Balance) = \(\beta_0\) + \(\beta_1 \times\)Student+ \(\beta_2 \times\)Income - Model 2: \(E\)(

Balance) = \(\beta_0\) + \(\beta_1 \times\)Student+ \(\beta_2 \times\)Income+ \(\beta_3 \times\)Student\(\times\)Income

Coding in R: Student=“No” is coded as 0 and the baseline, and Student=“Yes” as 1

Interaction terms: II

Interaction terms: II

Fit the model with interaction:

Call:

lm(formula = Balance ~ Student * Income, data = creditData)

Residuals:

Min 1Q Median 3Q Max

-773.39 -325.70 -41.13 321.65 814.04

Coefficients:

Estimate Std. Error t value Pr(>|t|)

(Intercept) 200.6232 33.6984 5.953 5.79e-09 ***

StudentYes 476.6758 104.3512 4.568 6.59e-06 ***

Income 6.2182 0.5921 10.502 < 2e-16 ***

StudentYes:Income -1.9992 1.7313 -1.155 0.249

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1

Residual standard error: 391.6 on 396 degrees of freedom

Multiple R-squared: 0.2799, Adjusted R-squared: 0.2744

F-statistic: 51.3 on 3 and 396 DF, p-value: < 2.2e-16Diagnostics

Diagnostics

- Diagnostics for multiple linear regression are very similar to those for simple linear regression with a quantitative predictor.

- Additional task: check on collinearity and variance inflaction factor (VIF)

Collinearity

Collinearity

- refers to the situation in which two or more predictor variables are closely related to each other

- often inflates the variances of estimated coefficients and makes the model unstable

- can be measured by the variance inflaction factor (VIF)

A VIF value that exceeds 5 or 10 indicates a problematic amount of collinearity

Note: VIF(\(\hat{\beta}_j) = \frac{1}{1-R^2_{X_j|X_{-j}}}\); collinearity implies \(R^2_{X_j|X_{-j}} \approx 1\)

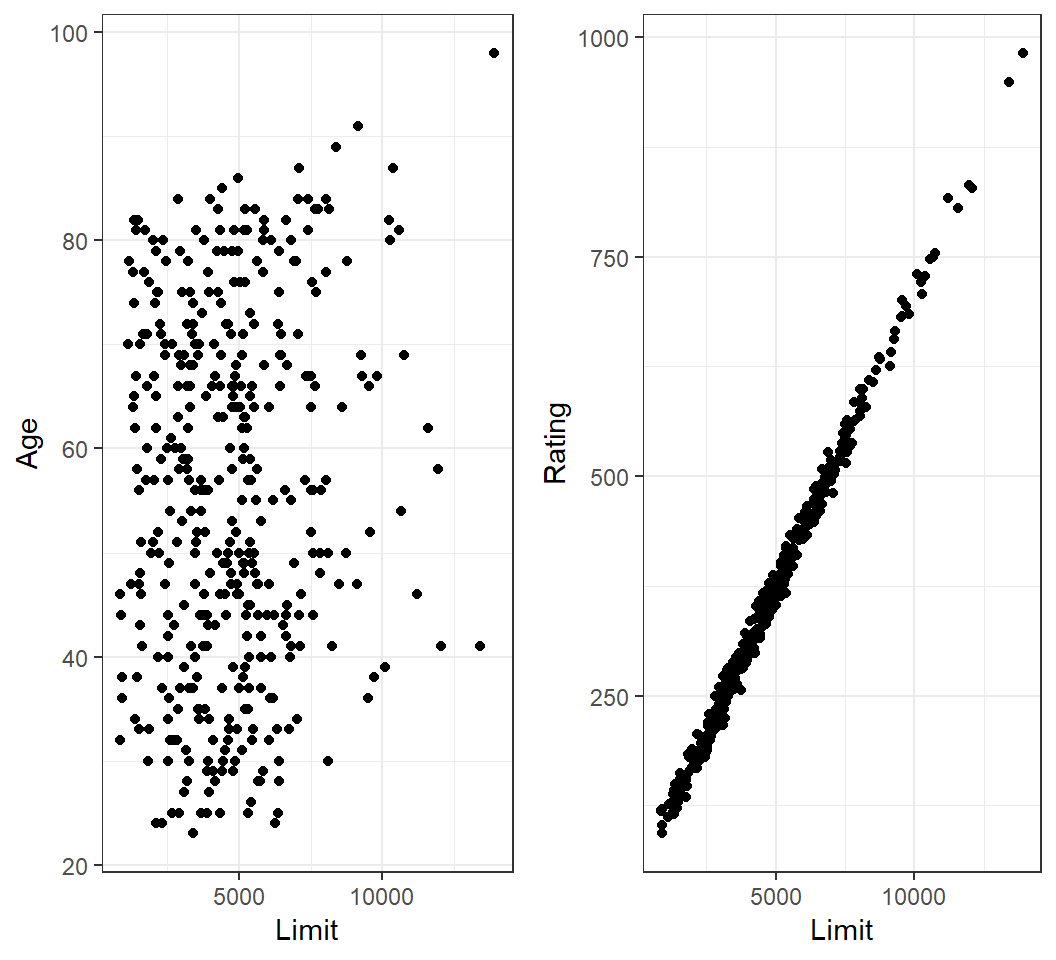

Collinearity

Collinearity among Limit and Rating:

Colllinearity

Model Balance~Age+Limit:

# A tibble: 3 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -173. 43.8 -3.96 9.01e- 5

2 Age -2.29 0.672 -3.41 7.23e- 4

3 Limit 0.173 0.00503 34.5 1.63e-121Model Balance~Rating+Limit:

# A tibble: 3 x 5

term estimate std.error statistic p.value

<chr> <dbl> <dbl> <dbl> <dbl>

1 (Intercept) -378. 45.3 -8.34 1.21e-15

2 Rating 2.20 0.952 2.31 2.13e- 2

3 Limit 0.0245 0.0638 0.384 7.01e- 1Note: compare standard errors of \(\hat{\beta}_{\textsf{Limit}}\) in both models

Colllinearity

> FitL3f = lm(Balance~Age+Rating+Limit,data=creditData)

> library(car)

> vif(FitL3f)

Age Rating Limit

1.011385 160.668301 160.592880 - VIFs indicate considerable collinearity in the data

In case of collinearity, either drop one of the problematic variables or combine some closely related variables

Non-linear models

Non-linear relationship

If there is evidence on a non-linear relationship between response and predictors, we can

- add high-order terms into the model (or employ more advanced non-linear methods); e.g., \[E(Y)=\beta_0+\beta_1 X + \beta_2 X^2\]

- transform predictors (and/or response); e.g., e.g., \(E(Y)=\beta_0+\beta_1 \times f(X)\), where \(f\) can be \(\log(X)\) or \(\sqrt{X}\)

License and session Information

> sessionInfo()

R version 3.5.0 (2018-04-23)

Platform: x86_64-w64-mingw32/x64 (64-bit)

Running under: Windows 10 x64 (build 19041)

Matrix products: default

locale:

[1] LC_COLLATE=English_United States.1252

[2] LC_CTYPE=English_United States.1252

[3] LC_MONETARY=English_United States.1252

[4] LC_NUMERIC=C

[5] LC_TIME=English_United States.1252

attached base packages:

[1] stats graphics grDevices utils datasets methods

[7] base

other attached packages:

[1] car_3.0-2 carData_3.0-2 broom_0.5.1 gridExtra_2.3

[5] ggplot2_3.1.0 knitr_1.21

loaded via a namespace (and not attached):

[1] revealjs_0.9 tidyselect_0.2.5 xfun_0.4

[4] purrr_0.2.5 haven_2.0.0 lattice_0.20-35

[7] colorspace_1.3-2 generics_0.0.2 htmltools_0.3.6

[10] yaml_2.2.0 utf8_1.1.4 rlang_0.4.4

[13] pillar_1.3.1 foreign_0.8-70 glue_1.3.0

[16] withr_2.1.2 readxl_1.2.0 plyr_1.8.4

[19] stringr_1.3.1 cellranger_1.1.0 munsell_0.5.0

[22] gtable_0.2.0 zip_1.0.0 evaluate_0.12

[25] labeling_0.3 rio_0.5.16 forcats_0.3.0

[28] curl_3.2 fansi_0.4.0 Rcpp_1.0.3

[31] scales_1.0.0 backports_1.1.3 abind_1.4-5

[34] hms_0.4.2 digest_0.6.18 openxlsx_4.1.0

[37] stringi_1.2.4 dplyr_0.8.4 grid_3.5.0

[40] cli_1.0.1 tools_3.5.0 magrittr_1.5

[43] lazyeval_0.2.1 tibble_2.1.3 crayon_1.3.4

[46] tidyr_0.8.2 pkgconfig_2.0.2 data.table_1.11.8

[49] assertthat_0.2.0 rmarkdown_1.11 rstudioapi_0.8

[52] R6_2.3.0 nlme_3.1-137 compiler_3.5.0